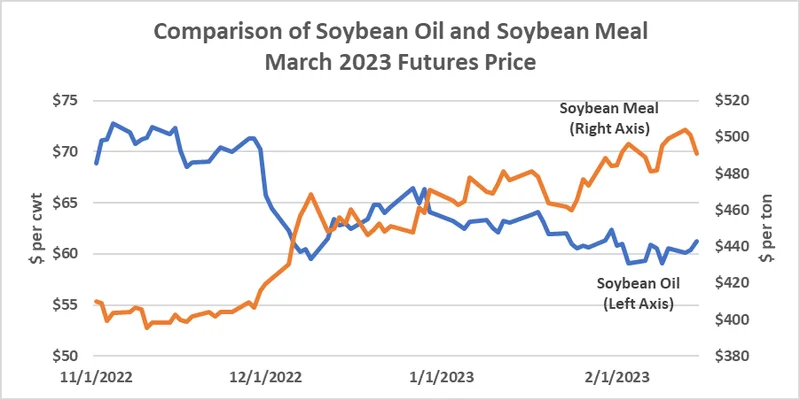

China's Soybean Deal: A Data-Driven Look at the Lifeline for U.S. Farmers

The reaction in the Chicago Board of Trade was immediate and predictable. Following U.S. Treasury Secretary Scott Bessent’s announcement of a trade truce with China, soybean futures surged. The numbers were, on the surface, impressive: a commitment from Beijing to purchase 12 million metric tons of U.S. soybeans this season, followed by a pledge to buy 25 million tons annually for the next three years. The most active soybean contract jumped 1.4%, touching a high of $11.14-1/2 a bushel—a level unseen since July 2024.

For farmers in places like Iowa, the nation’s second-largest soybean producer, the news was framed as a long-awaited rescue. "This is great news for Iowa farmers," declared Iowa Agriculture Secretary Mike Naig. Tom Adam, president of the Iowa Soybean Association, noted the deal "addresses many of the concerns around market access to China." China pledge of soybean purchases 'great news' for Iowa farmers, state ag secretary says.

The market, it seems, priced in a narrative of relief. After months of China pointedly ignoring American supplies amidst a broader trade standoff, this massive purchase order felt like the cavalry arriving. The initial price spike suggests traders believed this wasn't just a transaction, but a fundamental shift. But does this commitment truly alter the underlying economics for the American farmer, or is it a short-term sedative for a chronic condition?

The Anatomy of a Price Spike

Let’s be precise about the market’s reaction. The soybean contract didn’t just rise; it reversed an earlier fall, surging to a 15-month peak. The rally added about 45 cents to the market in a very short period—to be more exact, it was closer to 48 cents from the session's low to its peak. This wasn't a gentle updraft; it was a rocket fueled by a single announcement. The immediate cause was the alleviation of uncertainty. For months, the market had been operating in a vacuum, with initial readouts from U.S.-China meetings lacking concrete details. Bessent’s statement provided hard numbers, and capital markets abhor a vacuum.

The deal itself represents a significant volume. To put 25 million metric tons into perspective, it’s a substantial portion of the U.S. export program. If China follows through, analysts at CM Navigator project that Chinese demand for U.S. soybeans could return to 2023/24 levels by the 2026/27 season. This is the data point that officials are clinging to. It’s a clean, linear projection that suggests a return to normalcy.

But I've looked at hundreds of these market-moving announcements, and the initial euphoria often obscures a more complicated reality. The price action is a vote of confidence in the deal's execution, but it's not an audit of the entire agricultural balance sheet. Is this massive purchase order an economic game-changer, or is it like pouring a bucket of fresh water into a flooding river? It might feel significant at the point of entry, but does it actually lower the overall water level?

A Dissenting View from the Balance Sheet

While the soybean pits in Chicago were celebrating, a far more sober analysis was being presented by Rabobank. Their forecast paints a picture not of recovery, but of a prolonged downturn. The core of their argument is a simple, brutal equation: global supply is overwhelming global demand, even with China’s renewed appetite. They don’t see much potential for American farmers to break even until the 2027-28 crop year. That’s a long time to be underwater. Corn soybean farmers face years of low prices.

The problem is one of abundance. Years of bumper harvests in the U.S., South America, and elsewhere have created what Rabobank’s Stephen Nicholson calls "monster supplies." Consider the U.S. corn crop, which is expected to exceed 16 billion bushels for the first time in history. Even with record exports, stockpiles are projected to swell above 2 billion bushels, a seven-year high. While this isn't soybeans, the grain markets are deeply interconnected; a glut in one puts downward pressure on the others.

This is the part of the analysis I find most compelling because it divorces the geopolitical narrative from the physical reality of supply and demand. The China deal is a significant demand-side event, but it’s running headfirst into a historic supply-side glut. At the same time, the costs farmers face are not receding. Input prices for things like fertilizer and seed "have been very, very sticky," according to Nicholson. They rose sharply in previous years and have refused to come down at the same rate as crop prices (a classic case of price asymmetry).

So, farmers are caught in a vise. The price they receive for their product is being suppressed by global oversupply, while the cost to produce it remains historically high. The Rabobank report suggests that to truly bring the market back into balance, the U.S. may need to take another 3 to 5 million acres of principal crops out of production. Think about that. The market may require a deliberate contraction of the American agricultural footprint to restore profitability. If that forecast holds, what does this one-off Chinese purchase agreement truly solve in the long run?

The Signal vs. The Noise

My analysis suggests we're witnessing a classic market divergence. The futures market is reacting to a strong, clear "signal"—a multi-year, multi-billion-dollar purchase agreement from the world's largest soybean importer. It's a tangible piece of good news, and it's being priced in accordingly.

But the underlying "noise" of the broader agricultural economy hasn't changed. The world is still awash in grain. Production costs are still stubbornly high. The fundamental profitability equation for the individual farmer remains deeply challenged. The China deal provides a desperately needed destination for millions of tons of American soybeans, which will certainly help clear some of this year's inventory. It is, without question, better than no deal at all.

However, mistaking this lifeline for a cure would be a significant analytical error. It doesn't solve the systemic overproduction problem, nor does it alleviate the pressure of high input costs. The Rabobank forecast, with its grim timeline for a return to breakeven, feels like a more grounded assessment of the long-term reality. The market's celebratory price spike is a vote for optimism, but the balance sheet is casting a vote for caution. For the American farmer, this deal may just mean the difference between a disastrous year and a merely difficult one.