The Great Mortgage Rate Drift: Why the Fed's Moves Aren't Reaching Your Wallet

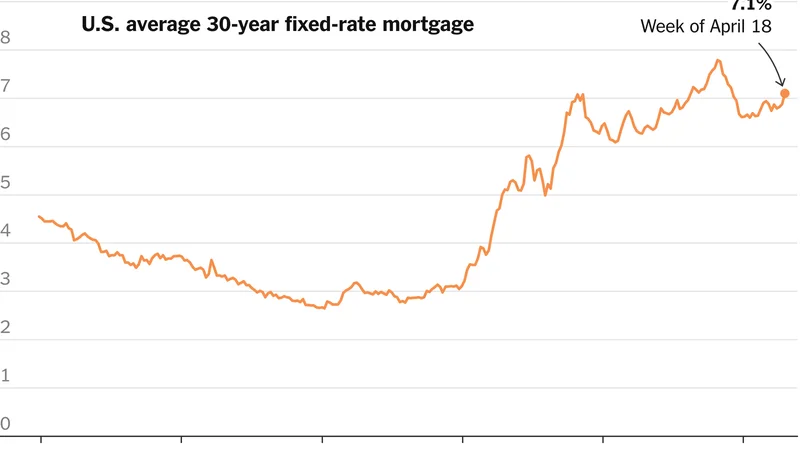

The numbers out this week are, for lack of a better word, inert. As of October 29, 2025, the average 30-year fixed-rate mortgage is hovering at 6.156%, according to Optimal Blue data. That’s a rounding error away from the day before and a single basis point higher than a week ago. Zillow’s competing data set pegs it at 6.16% (Current mortgage rates on October 29, 2025). Pick your source; the conclusion is the same. The market is treading water.

For the millions of prospective homebuyers sitting on the sidelines, staring at their Zillow tabs like ancient mariners watching a windless sea, this stasis is maddening. They were told a story: when the Federal Reserve starts cutting rates, borrowing gets cheaper. The Fed did deliver a quarter-point cut in September. They’re expected to cut twice more before the year is out. Yet, the relief hasn't trickled down to Main Street. The promised tailwind is little more than a whisper.

This disconnect isn't just a statistical anomaly; it's the central story of the 2025 housing market. The Fed is pressing the levers of monetary policy, but the machine isn't responding as expected. It's like trying to steer a massive cargo ship with a canoe paddle. The intention is there, but the underlying forces—inflationary ghosts, a murky labor market outlook under a new Trump administration, and the Fed’s own internal contradictions—are creating a current too strong to overcome. We've been conditioned to watch the Fed's every move, but right now, that feels like watching the wrong show.

The Fed's Phantom Signal

Let’s be precise. The expectation that mortgage rates would ease when the Federal Reserve began cutting the federal funds rate wasn’t just wishful thinking; it was based on decades of economic precedent. But that precedent is failing us. We saw a brief dip in rates leading up to the September 2024 Fed meeting, only for them to rebound almost immediately. Fast forward to January 2025, and the 30-year average breached 7% for the first time since the prior May, a jarring figure when the memory of 2.65% from January 2021 is still so fresh.

The problem lies in a fundamental misunderstanding, amplified by financial media, of how mortgage rates are actually set. The federal funds rate is an overnight bank-to-bank lending rate. It’s a short-term instrument. Mortgages, on the other hand, are long-term products priced against instruments like the 10-year Treasury yield, which is far more sensitive to long-term inflation expectations and overall economic health.

And this is the part of the analysis that I find genuinely puzzling. Everyone is fixated on the Fed's rate cuts while largely ignoring the more powerful tool at its disposal: its balance sheet. During the pandemic, the Fed bought mortgage-backed securities (MBS) by the truckload to inject liquidity into the system. Now, it's been shrinking its balance sheet, letting those assets mature without replacing them. This process, known as quantitative tightening, effectively pulls money out of the mortgage market, creating upward pressure on rates. The Fed is stepping on the accelerator with rate cuts and the brake with its balance sheet simultaneously. Why are we surprised the car is just shuddering in place? Which of these two opposing forces is the true indicator of the Fed's intent? And why does one get all the headlines while the other operates in relative obscurity?

A Market of Contradictions

Digging into the week-over-week data reveals a market that isn't just stagnant, but internally inconsistent. The 30-year conventional rate barely budged. Yet, the 30-year jumbo rate, for larger loans, jumped from 6.336% to 6.531% in a single week according to one data set, before falling back to 6.442% a day later. That’s not a drift; it’s a spasm. Meanwhile, government-backed loans show their own logic, with VA and USDA rates dipping nicely below 6%. It’s a fractured landscape where your borrowing cost depends entirely on which slice of the market you occupy.

This volatility is layered on top of a larger psychological trap: the "golden handcuffs." The historical charts tell us that 6% or 7% rates aren't an aberration. In October 1981, the average rate was a staggering 18.45%. But historical context is little comfort to someone who bought or refinanced at 2.8% in 2021. Those homeowners are now effectively locked in place. They can't sell and move without doubling their monthly housing payment, which has frozen a huge chunk of housing inventory and is propping up prices even as affordability craters.

The result is a standoff. Buyers can't afford the monthly payments at current rates and prices. Sellers with low-rate mortgages can't afford to move. The only real activity is in the new construction market, where builders can offer rate buydowns (a marketing gimmick where they subsidize the mortgage rate for a few years) to create the illusion of affordability. It’s a temporary fix for a systemic problem. We have to ask: what is the long-term economic consequence of having an entire generation of homeowners immobilized? Does this create a permanent drag on labor mobility and economic dynamism?

The advice given to prospective buyers in this environment is frustratingly generic: boost your credit score, lower your debt-to-income ratio, shop around. And while that’s sound financial hygiene—a credit score of 740 or higher is non-negotiable for the best rates—it feels hopelessly inadequate. It's like telling someone to bring a bucket to a house fire. Yes, it’s better than nothing, but it completely misses the scale of the problem. The issue isn't just individual financial readiness; it's a market that has lost its directional compass.

The Signal Has Become the Noise

My analysis suggests we’re in a period of sustained ambiguity. The market isn't reacting to the Fed's forward guidance because that guidance is contradictory. The Fed is cutting short-term rates to stave off a recession while simultaneously tightening the long-term credit supply with its balance sheet. One is a public performance; the other is a structural reality. Watching the federal funds rate for a clear signal on mortgages is, for the foreseeable future, a fool's errand. The real story isn't the rate itself, but the chaotic interplay of inflation fears, national debt, and a central bank that appears to be at war with itself. For the average homebuyer, that means the drift will continue until one of these larger forces decisively wins. Don't watch the Fed's lips; watch its balance sheet. That’s where the truth is.